I would motivate you to contact an estate lawyer to be sure whatever remains in order now though while mom is still able to sign additional documents if needed. It is totally approximately you and also there are no adverse implications for paying at weird periods or simultaneously. I would highly suggest you get in touch with a loan provider before you do anything else to establish the cleanest way to complete the deal. Otherwise till after, he will certainly be required to also experience a great deal of the documentation and also the therapy.

If you. proceed, the documents can be signed and also returned for negotiation. It is essential that you are completely delighted with all facets of http://gunnerwvpw725.timeforchangecounselling.com/fha-lendings your Heartland Opposite Mortgage. To guarantee this, the lawful suggestions on your loan contract should be carried out by a solicitor of your choice, that will certainly represent your passions and also work with you to discuss and also discuss your financing.

- Reverse mortgages are likewise high-risk in terms of rip-offs, and numerous customers fall victim to predative practices that can cost them substantial quantities of cash or the house itself.

- Unlike with a typical home loan, where you make monthly repayments to pay for your funding, with a reverse home loan, you're the one obtaining settlements from the lender.

- You do not need to make any lending payments till completion of the loan.

- This indicates that you still need to pay property taxes, keep threat insurance policy and keep your house in great repair work.

This is usually done when you intend to relocate into a brand-new house, however don't wish to wait up until your existing residence is sold to do so. If you're not marketed on getting a reverse home loan, you have choices. Actually, if you're not yet 62, a home equity loan or HELOC is likely a better option.

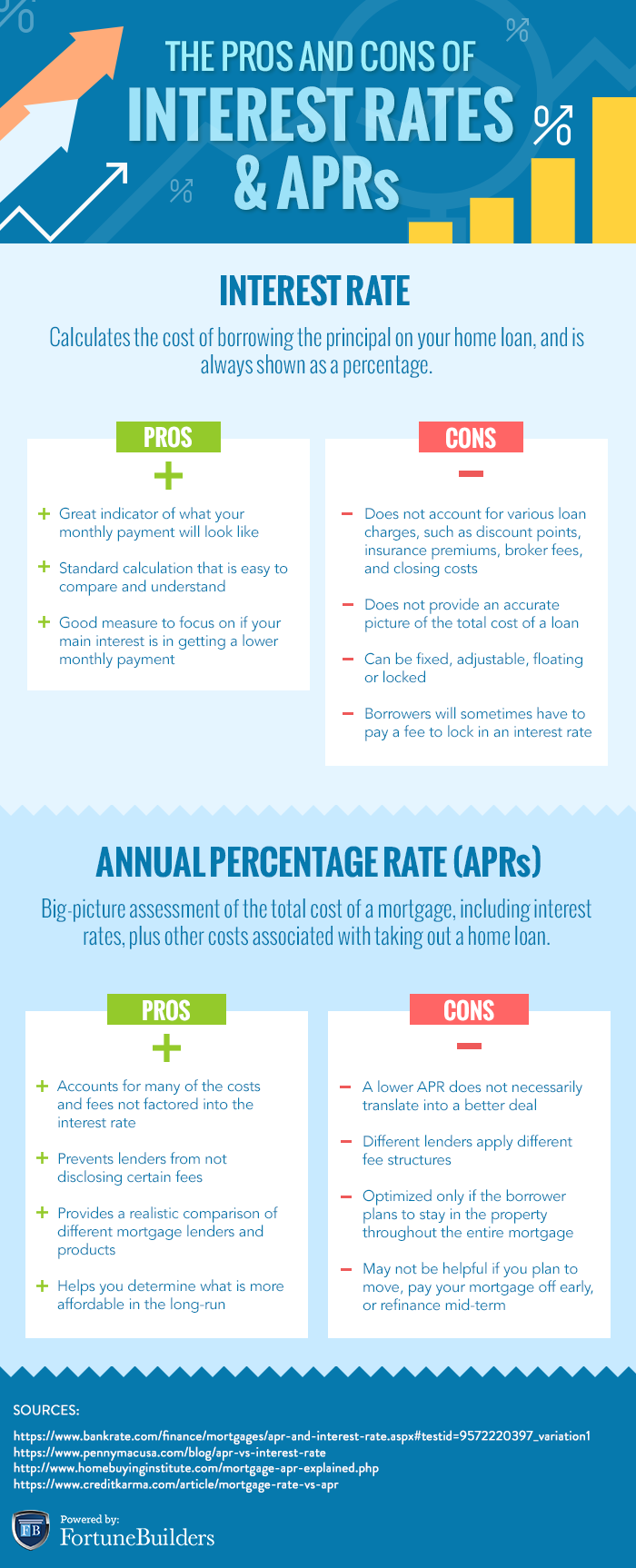

Regular Monthly Passion Charges

A reverse home loan might limit other financing choices secured by your house. If both partners get on the lending or one partner is out the lending but is an "eligible non-borrowing partner" after that indeed, either partner can continue to be in the home for life also after the other spouse passes with a reverse home mortgage. The reverse home mortgage supplies several different options to access the offered funds. Recognizing bluegreen timeshare cancellation policy what you want out of your reverse home loan will certainly aid you choose the very best option to meet your long and also short term goals. So, she acquires her reverse home loan and-- after the expenses to acquire the car loan-- has the very same $200,000 credit line offered to her. If there are multiple consumers, the age of the youngest customer will decrease the amount offered since the terms permit all consumers to live in the house for the rest of their lives without needing to make a repayment.

Just How Do You Repay A Reverse Home Mortgage?

Depending on the type of car loan you select and exactly how you handle your money, you might outlive your earnings. Although there are a number of benefits that include a reverse home loan, the loan can likewise have some points that you will intend to think about. There are no credit rating demands at this time, though credit rating will be assessed throughout a monetary analysis. It additionally secures you from losing your funding if your lender goes out of business or can no more fulfill its obligations for whatever reason.

By the fiscal year finishing in September 2008, the yearly quantity of HECM fundings topped 112,000 representing a 1,300% rise in 6 years. For the ending September 2011, lending quantity had contracted in the wake of the financial situation, but stayed at over 73,000 loans that were stemmed and also guaranteed with the HECM program. If you believe a fraud, or that someone involved in the deal might be damaging the legislation, let the counselor, lender, or lending servicer know. Then, file a problem with the Federal Profession Payment, your state Chief law officer's office, or your state banking regulatory company. Just how much you can actually The original source borrow is based on what's called the preliminary primary restriction.

Some hail the reverse mortgage as a reasonable remedy for retired people who require extra money, enabling them to use what is most likely their most useful possession. Be aware that given that the house will likely require to be sold to repay the reverse home loan, these types of loans may not be an excellent choice if you want to leave your home to your youngsters. You as well as any kind of other consumers on the reverse home mortgage need to be at least 62 years of age. If you certify, these programs are a better option than getting one more kind of reverse home loan.

For individuals that want more revenue than what Superannuation supplies them, they may pick to take a reverse home mortgage to supplement their pay. A reverse home mortgage can be paid in a lump sum of money or in routine instalments. Relying on your age, you can borrow 15-40% of your house's existing value. Unless you select the round figure option, your reverse mortgage interest rate is adjustable, which can promptly lower your offered equity if rates get on the increase. If you have a high-value residence, you may need to take this kind of financing to borrow even more funds.

When working with a private loan provider-- and even an exclusive company that claims to broker federal government financings-- it is essential for debtors to be cautious. Once the consumer picks a details loan program, they make an application for the finance. The lender does a credit report check, assesses the debtor's property, its title and assessed worth. If approved, the lender funds the lending, with proceeds structured as either a round figure, a line of credit or regular annuity settlements, relying on what the borrower picks. Comparable to loan-to-value in the forward home loan globe, the principal limit is essentially the portion of the worth of the residence that can be lent under the FHA HECM standards. Most PLs are normally in the series of 50% to 60% of the MCA, yet they can in some cases be higher or lower.